Privately Owned Insurance Companies (POIC): A Business Owner's Guide

A Privately Owned Insurance Company (POIC) is a legal, IRS-compliant insurance company you own that insures your business’s own uninsured and under-insured risks. Instead of paying premiums to an outside carrier and never seeing that money again, you keep the underwriting profit — net of any claims — inside a company you control.

For middle-market business owners, a POIC turns a recurring cost into a long-term asset. This guide explains what a POIC is, how it works, what it covers, how it compares to a captive, and how Reinsurance Specialties implements it through The Latitude Plan.

Private insurance for the middle market

For decades, large corporations have used private insurance and alternative risk transfer to manage risk, reduce insurance costs, and capture underwriting profit — and the capital behind that market is at an all-time high, with global reinsurer capital reaching a record $785 billion at the end of 2025 (Aon). Today that same strategy is available to middle-market companies. Reinsurance Specialties serves business leaders nationwide — with clients in 30 U.S. states and growing — across virtually every industry.

What is a privately owned insurance company (POIC)?

A privately owned insurance company (POIC) is a closely held insurance company formed primarily to insure the uninsured and under-insured risks of its owner and affiliated businesses. As the owner, you are involved in the operations that matter: underwriting, policy placement, claims decisions, investments, and annual strategy.

A POIC re-insures risks that your standard commercial policies leave exposed. It doesn’t replace your commercial property and casualty coverage — it sits on top of it, covering the gaps that traditional carriers avoid or overprice.

How did private insurance become available to the middle market?

Private insurance isn’t new. Self-insurance dates back to the 1600s; the modern reinsurance platforms that anchor today’s market formed in Bermuda in the 1960s and were formalized in the late 1970s — including an early structure built around Harvard University’s medical malpractice exposure. Federal risk-retention legislation followed in 1986.

What changed for smaller companies was access, not the concept. Until 2001, IRS regulations effectively kept these structures out of reach for middle-market businesses. A series of IRS “safe harbor” rulings in 2001, 2002, and 2005 established the framework that made compliant private insurance practical for privately held companies.

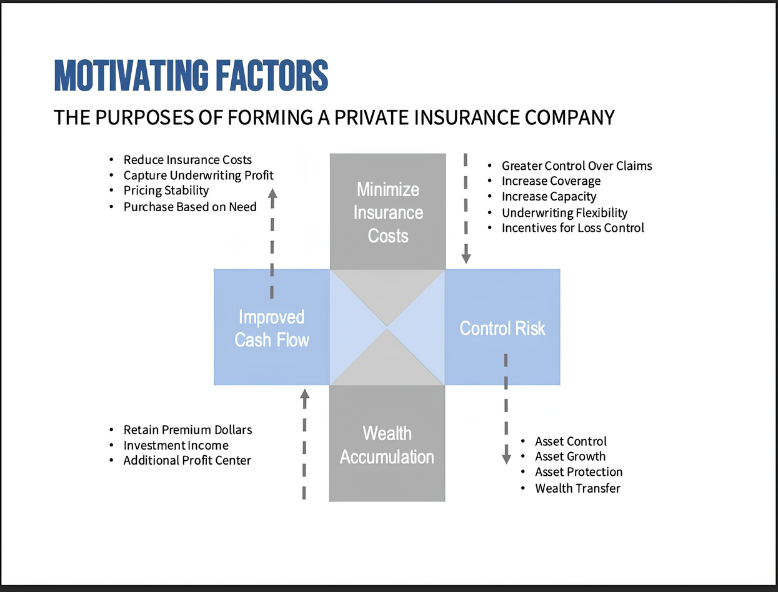

Why business owners form a POIC

Forming a privately owned insurance company through The Latitude Plan lets a business retain underwriting profits, gain control over claims, and tailor coverage for risks that are otherwise hard to place. It supports tax-efficient reserve planning, improved cash flow, and investment strategies aligned with growth and M&A — converting insurance premiums into company-controlled assets.

Financial advantages

Retain underwriting profits and investment income, access potential tax benefits, and lower administrative costs compared with conventional commercial insurance.

Strategic flexibility

Gain access to premium and the ability to cover risks that traditional carriers may avoid or overprice.

Operational control

Direct control over claims management and risk management, plus the ability to customize policy language for niche or hard-to-place risks.

Long-term value

Build equity through an insurance vehicle that can serve as a profit center, separate from your operating businesses.

How business owners use a POIC

Business leaders across every industry use private insurance to mitigate risk, control claims, improve cash flow, protect assets, and build long-term, transferable wealth — all within a compliant insurance framework. Here are common, solutions-based applications:

Specialized coverage

Hard-to-place coverage such as business interruption or comprehensive Directors & Officers can be obtained at reasonable, consistent rates.

Creditors & finance

Finance organizations can underwrite creditor/insured coverage such as collateral protection, vendor single-interest, and other credit risks.

Construction

A POIC can re-insure subcontractor default, construction defects, mold, and other construction-related general liability, improving the cash flow and profitability of the general contractor or developer.

Medical malpractice

Hospitals, physician groups, and medical professionals can self-insure all or part of malpractice risk, capturing underwriting profit and achieving better loss and claims control.

Property coverage

Large property holders can re-insure completed coverage or different layers of property risk, reducing overall insurance cost.

Non-traditional lines

A POIC can re-insure coverages like equipment-maintenance warranty, credit life and disability, employment practices, credit risk, post-retirement medical benefits, extended-service warranty, voluntary employee benefits, pollution liability, and medical stop-loss.

What's the difference between a POIC, a captive, and an 831(b) micro-captive?

These terms overlap, which causes confusion. Here’s the plain-language version:

Captive insurance is the broad category: an insurance company owned by the business it insures. The term dates to 1955. A POIC is a modern form of captive.

An 831(b) micro-captive is a specific tax election that the IRS has scrutinized heavily for abusive tax sheltering. Poorly designed or ill-intended micro-captives have drawn audits and penalties.

The Latitude Plan is a POIC structured under an 831(a) designation — not an 831(b) micro-captive. It uses a simple, linear transfer of risk by policy and treaty, files annual federal tax returns, and deliberately excludes the elements associated with IRS scrutiny: no 831(b) election, no offshore accounts, no risk pooling, and no trust agreements.

The Latitude Plan — our POIC structure

By now you can see the flexibility of a privately owned insurance company. The Latitude Plan is how Reinsurance Specialties puts it to work — a POIC structure refined over nearly three decades. Two things set it apart from conventional captive and private-insurance models:

Sovereign tribal domicile. Your POIC is formed under the legal jurisdiction of a federally recognized Native American tribe, supported by the Indian Reorganization Act of 1934 — not a U.S. state or an offshore territory. Because it isn’t filed with any Secretary of State, your accumulated premium reserves stay off searchable public registries, helping shield them from creditors and litigators. It also avoids state audits, investment restrictions, and the commissioner-approval requirements that state-chartered captives face.

An 831(a) designation, not a scrutinized micro-captive. The Latitude Plan operates under an 831(a) designation and files annual federal tax returns. It is deliberately designed to exclude the elements that draw IRS scrutiny — no 831(b) micro-captive election, no offshore accounts, no risk pooling, no trust agreements, and no outside administrators.

What business leaders say

"We vetted many servicing companies before landing on this reinsurance platform. They have been extremely helpful in introduction, education, and connections with third-party operational teams."

Jeff M., Florida

"Reinsurance is a beautiful business tool used to help control business risk exposures surrounding our ten LLCs; we remit tax-advantaged premium monthly and enjoy mitigating our collective risks."

Morgan J., New York

"Reinsurance Specialties has surrounded itself with subject-matter experts who bring education, actuarial assessment samples, case studies, and insights to the table. The onboarding with the third-party insurer was simple and straightforward."

Rick W., Florida

CONTACT REINSURANCE SPECIALTIES™

Email: info@reinsurancespecialties.com

For any general inquiries, please fill in the following contact form: